MEV, Canton and the fight over blockchain’s future.

The dominant L1 business model in 2026 is front-running your users.

That sounds inflammatory but it’s what the numbers say. Solana generates roughly $1.5 billion in annual revenue. About $100 million of that comes from base fees. The rest, the overwhelming majority, comes from priority fees and MEV. Priority fees are what users pay to get their transactions processed ahead of others. MEV is what sophisticated actors extract by reordering those transactions to their advantage. The business model works when transactions compete for scarce blockspace, because competition creates contention, and contention is where the money is.

Bryan Pellegrino gave an unusually honest assessment of where things stand at Digital Asset Summit last week. Base fee revenue is dead. Throughput has been commoditized.

The game now is creating contentious blockspace and charging premiums for it. He’s right about the economics. @andyyy connected it to the Wilson clip and was honest enough to say what most people were thinking: “just not sure if ‘get the institutions onboard and MEV-sandwich retail’ is the endgame.”

If your protocol’s revenue depends on users fighting each other for position, you have a structural incentive to make that fight worse. More contention, more priority fees, more MEV, more revenue. The chains that extract the most from their users are the ones with the best business models. This is the system the industry built and is now defending as inevitable.

What institution is going to pay to migrate their settlement infrastructure onto rails where their transactions get sandwiched? What’s the efficiency gain at that point? You’ve reproduced the worst part of traditional market structure (order flow exploitation) on infrastructure that depends on this exploit and you’re calling it the future?

Don Wilson went further. MEV on public chains like Ethereum and Solana makes them unsuitable for financial markets, he argued at DAS. His solution: go permissioned. Use Canton, which he helped build through Digital Asset Holdings. On a permissioned chain with controlled participants and no public mempool, there’s no MEV.

He’s right about the problem. But Canton solves MEV the way a walled garden solves vandalism. You eliminated the problem by eliminating public access. The question is what you traded away to get there, and whether the thing you built is still doing what blockchains are supposed to do.

The critiques of Canton that surfaced this same week are worth reading in full. Swen Werner’s structural analysis (1, 2) argues that Canton’s cross-chain settlement is synthetic atomicity, that every counterparty relationship creates IT bottlenecks that don’t exist in traditional systems and that assets can’t be independently verified without the issuer’s permission. If a tokenized bond only exists because the issuer says it does, what exactly did the blockchain add? Alex Gluchowski applied a redundancy framework and concluded that Canton’s integrity model has a single mechanism with no independent verification layer. If operator keys get compromised, manipulated state propagates silently. MetaLeX published a thorough legal analysis calling most tokenized securities “intermediary cosplay”, institutions dressed in smart contract costumes still doing the same thing they did before blockchain.

Canton has $9 trillion in monthly volume and Goldman Sachs on its cap table. These are real numbers. But you don’t solve institutional adoption by trading one set of dealbreakers for another.

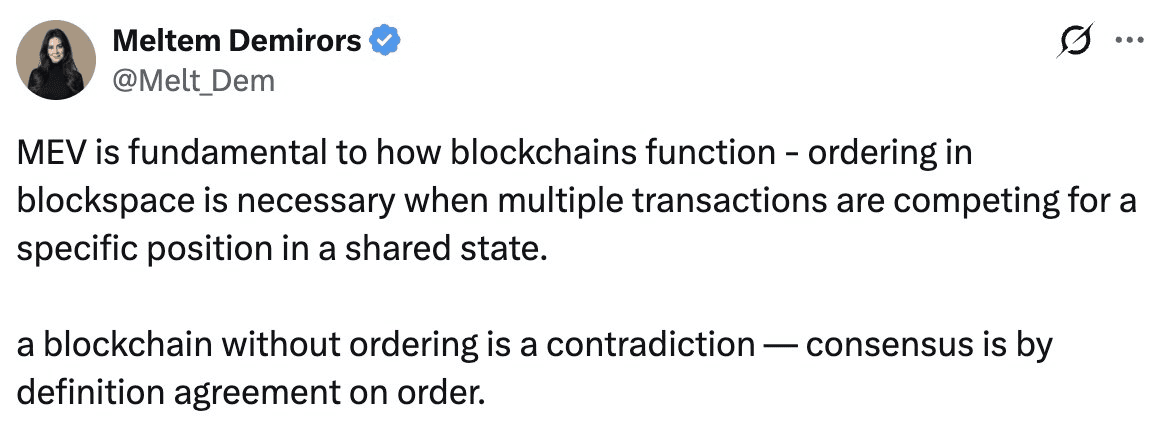

So the industry arrived at two camps. Public chains that extract value from users. Private chains that give up everything public infrastructure was supposed to provide. Rebecca Rettig at Jito Labs made the historical point: permissioned chains have been tried in at least two prior cycles and haven’t worked. @Melt_Dem made the technical point: MEV is fundamental to how blockchains work because consensus is by definition agreement on order, and ordering creates extractable value.

Meltem’s argument is technically correct. On chains where transactions compete for blockspace, ordering is necessary, and wherever there’s ordering there’s value in controlling that order. MEV follows from blockspace contention the way heat follows from friction.

But she also pointed out in the replies that this isn’t a crypto invention. HFTs do the same thing in equities. They fund their own compute and connectivity to reduce latency, ensuring their orders process first. Market makers front-run order flow in traditional finance every day. It’s why you trade for free on Robinhood. So the same institutions Wilson is trying to protect from MEV on public chains have been profiting from a version of it in traditional markets for decades. The only difference is transparency. On public chains it happens where everyone can see it. In traditional finance it happens behind dark pools and payment-for-order-flow arrangements.

Which makes Wilson’s argument even weaker. He’s not objecting to front-running. He’s objecting to front-running he can’t control.

But none of this changes the fact that for institutional adoption of public blockchain infrastructure, MEV is a real barrier. A central bank isn’t going to issue a digital currency on a chain where transactions get reordered for profit. A securities depository isn’t going to settle trades on infrastructure where the settlement layer’s business model depends on extracting value from the settlement process itself. The problem is real even if the people complaining about it loudest have self-interested reasons for doing so.

The assumption everyone in this debate shared, across every camp, is that on public blockchains, blockspace contention is a given. It’s how consensus works. You either accept it and build around it, or you go private to avoid it. Those are the options.

We disagree. Competition for blockspace is a design choice.

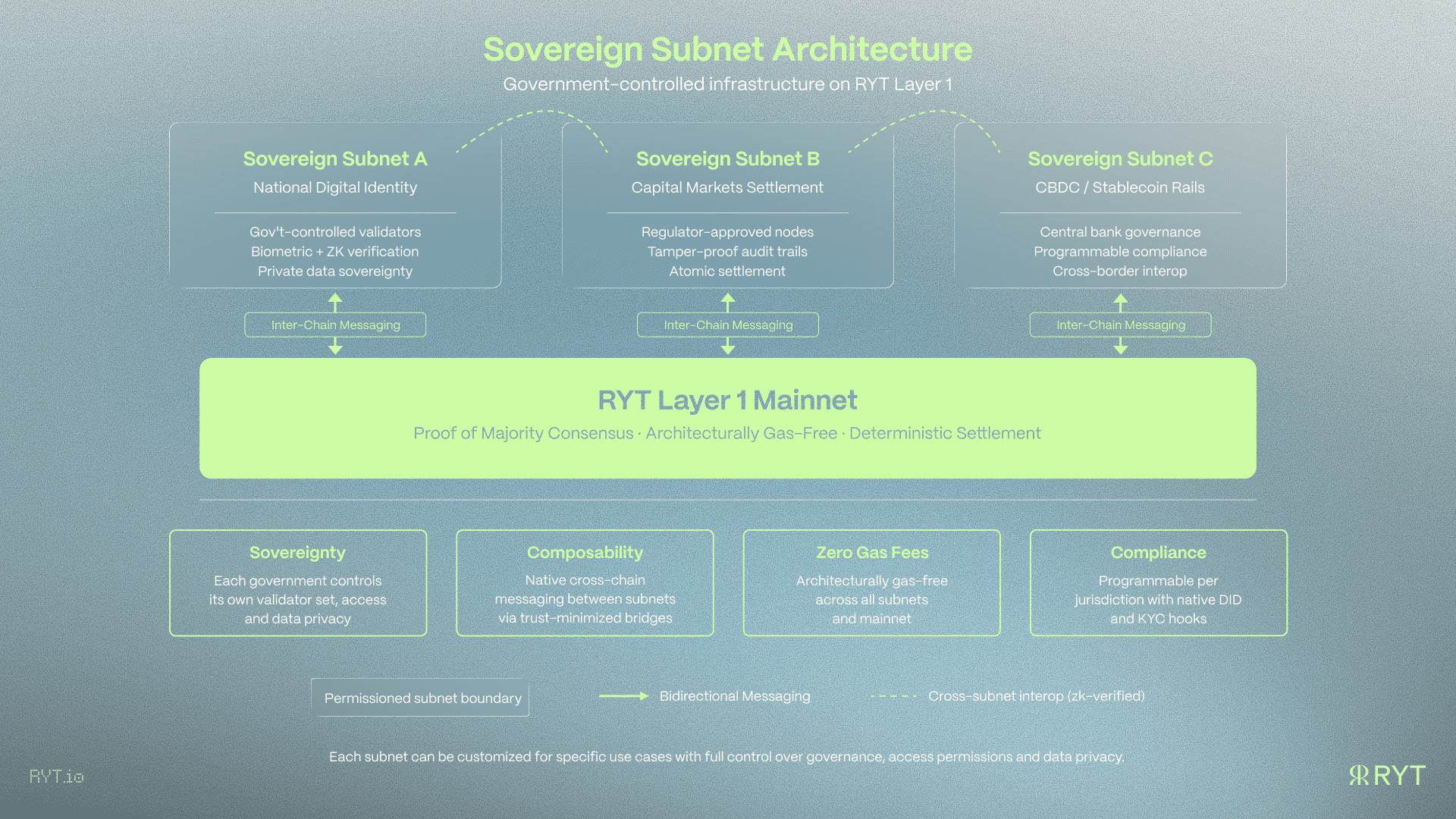

Proof of Majority, RYT’s patented consensus mechanism, eliminates blockspace contention entirely. Every node independently constructs a candidate block from unconfirmed transactions. Nodes gossip block hashes and finalize once a simple majority is observed. No leader election, no block proposer controlling transaction ordering. Every valid transaction is automatically included without competing for position, because there is no scarce blockspace to compete over. No blockspace contention means no ordering problem. No ordering problem means no MEV. Architecturally gas-free, deterministic settlement, on a public chain.

Sovereign subnets address the other half of the debate. Institutions that need private infrastructure deploy their own subnet with their own validators, governance rules and privacy controls. Those subnets connect to each other via zk-verified interop and to the public mainnet via inter-chain messaging. Credentials, assets and state verified on a sovereign subnet compose with the broader public ecosystem. You get the control Canton promises without abandoning public infrastructure. Privacy where you need it. Composability where you want it. Both on the same network.

Revenue is the obvious question. If a chain is architecturally gas-free and has no MEV, where does protocol revenue come from? The fact that the industry defaults to “extract MEV” as the answer says more about a lack of imagination than about economic necessity. Imagine a model where the chain stays free for end-user transactions and revenue comes from businesses and institutions who benefit from the network effects of a free-to-use ecosystem. Things like smart contract bonds from commercial users and value extractors or subnet deployments for institutions. Revenue generated at the application layer by entities that profit from frictionless user access, rather than extracted at the protocol layer from users who have no choice but to pay.

There are ways to sustain a chain without making your users the product. The industry hasn’t explored them seriously because the MEV model was printing money.

We should be honest about where we are. RYT is pre-revenue and pre-production. We’re building for governments across LATAM and MENA with active relationships in Pakistan, Panama and Costa Rica, but we haven’t shipped a production deployment. Canton has Goldman and $9 trillion in volume. Solana has BlackRock and years of battle-tested infrastructure. We’re not in the same weight class today.

But the architecture question isn’t about weight class. Either blockspace contention is a necessary property of all public blockchains, or it’s a design choice that some consensus mechanisms make and others don’t. If it’s a design choice, then the entire debate last week was arguing within a constraint that doesn’t need to exist. Public chains that don’t extract from users and private chains that aren’t private are both possible. The binary the industry is stuck in is a product of the architectures that exist today, not a law of how blockchains have to work.

We think the debate at DAS was one of the more important conversations this industry has had recently. We also think it stopped one step short of the conclusion that matters.